Rolling Reserve And What To Do About Them

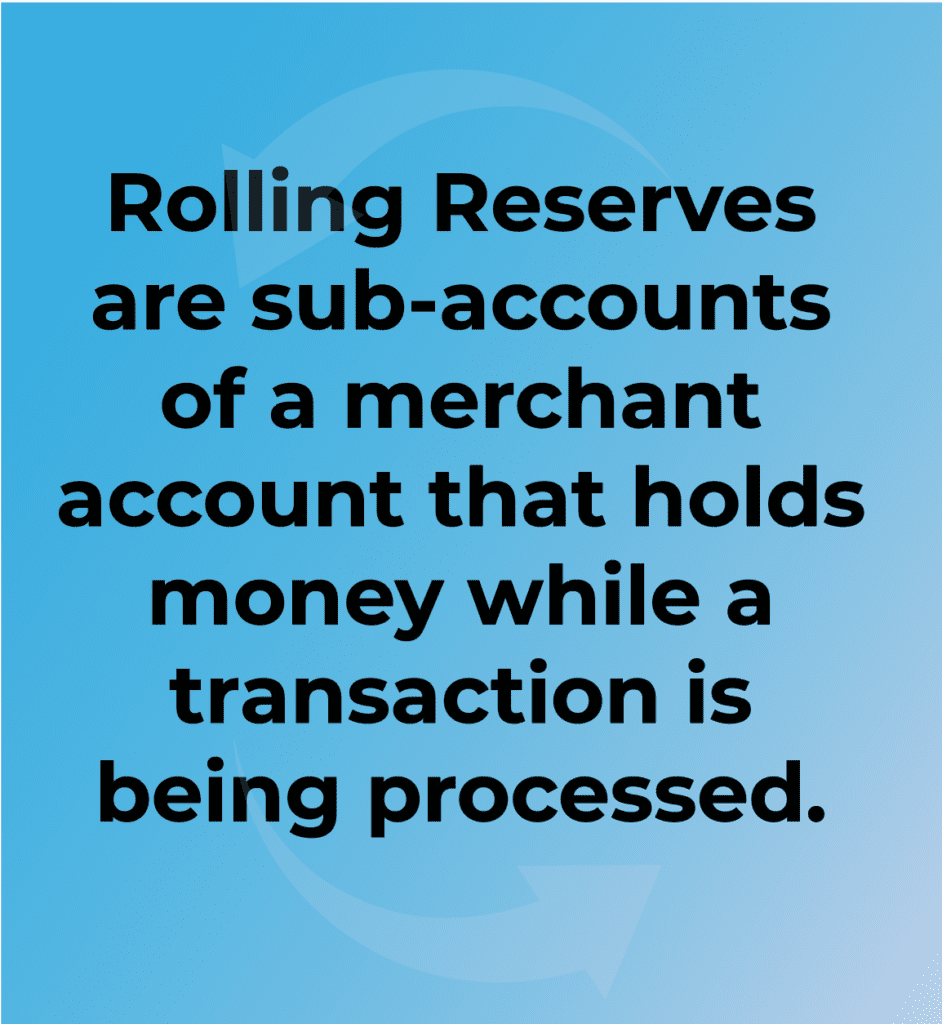

Before we get started on today’s topic, we need to answer this question: what is a rolling reserve? A rolling reserve on a merchant account will hold a percentage of your sales with your processor to be released at a later date. A reserve acts as a buffer to protect you, your customers and your merchant service provider from future chargebacks and disputes. Very few businesses want a rolling reserve; instead, they are often placed on an account by a merchant service provider.

You might have seen them in the news recently because of changes that were made to many MSP accounts. With the pandemic overtaking most of the United States, there was an influx of chargebacks. Service providers took defensive measures to protect themselves from exposure. The easy move for some providers was to add a reserve on certain industries altogether. Travel businesses were hit especially hard, but even if you were shipping cookies you might have run into issues.

If you landed on this article, you’ve probably been suffering from this. If you want our coverage of those specific issues, our article on them is here. However, rolling reserves aren’t an isolated issue. This is what you need to know about them, and what you can do to affect them.

Why Do Payment Processing Rolling Reserves Happen?

Merchant service providers add rolling reserves to an account for one reason: they anticipate the account having a lot of chargebacks. Chargebacks can get complicated pretty quickly, as you probably know if you’ve ever been on any side of one. Since it’s your processor’s job to return lost funds, they’re always evaluating their exposure on disputes.

A rolling reserve makes this simpler. The idea is that as long as the money is held in reserve, they won’t open themselves up to any risk. If a chargeback is filed, the processor drops into the reserve balance, return the funds to the issuing bank and removes the charge from your customer’s credit card bill. All without your business needing to return funds.

This can, of course, lead to issues for your business. Your cashflow will suddenly tighten, and you’ll be waiting much longer for your receivables to be paid out. If you’re waiting for money to come in for a long period, your flexibility gets hurt. This is especially true with the emergency reserves, which were originally unclear on when they would be released. There has also been an increase in false flags. Reserves can get added to businesses that don’t need them or aren’t actually high-risk.

Can You Remove Rolling Reserves?

So, you’ve been slapped with a reserve. Or you need one for your account to get approved. You can get it removed, right?

Well, yes and no.

What you have to figure out is why your Merchant Service Provider has placed one on your account. Is there something that happened that put you specifically in this place?

For sweeping, COVID-type reserves, it might be a hard no from companies like PayPal and Square. There isn’t going to be much room for negotiation, regardless of what you do. The best option in these cases is to look for other options.

But if you’re – for example – in an industry which has been deemed high-risk even though you aren’t, then you might be able to work something out.

Another common situation happens when the sales volume of a business skyrockets. An eCommerce startup might start doing sales volume very quickly that will look sketchy to a payment processor. For these businesses, waiting is the name of the game.

Rolling reserves are typically based on a business or an industry’s sales history. If you can build a good sales history over the course of a handful of months or even years, then you should be in good standing. This will often automatically take the reserve away, or give you negotiating power to get the reserve lifted.

If your business has been in good standing but suffered from a recent spike, you should already have some of that power. You will often be able to work with your Merchant Service Provider to arrange the terms of the reserve.

Unfortunately, in certain cases, payment aggregators like PayPal and Square can make broad stroke risk decisions that may group together high and low-risk merchants because they are in the same industry. This leads to businesses in good standing having reserves place on their account.

What Can I Do About Rolling Reserves?

The best solution to rolling reserves is to talk to your Merchant Service Provider and see what they care about. Why have they pegged you as a high-risk account? What metrics are they paying attention to? If you can learn what’s affecting the rolling reserve, then you can start to make change based on those metrics. This should loosen up the issue somewhat.

Remember that if you aren’t satisfied with these solutions, your hand isn’t forced in choosing your MSP. PayPal and Stripe might be the easy answer, but they aren’t the only answer. There are plenty of businesses that will help provide you with payment solutions. Finding the right business for doing so is a bit of a labyrinthine task, but it’s not unmanageable.

It’s important to find a flexible MSP that understands and wants your business. This will create more negotiating room in the details of your payment processing, and allow a solution to be found to any potential problems. Payment Processors aren’t as scary as they look, and will often enjoy working with you.

If you’re looking to solve MSP issues, we can make the solution a little bit easier.

Reach out to us at Direct Payment Group today to get set up with an account that will meet your needs first, and make sure your business runs smoothly.